We would like to inform you about a significant revision by Japan Customs, which clarifies the definition of an Importer. This change took effect on October 1, 2023.

With the revision, there has been an increase in cases where foreign corporations must use an Attorney for Customs Procedures (ACP) to become an Importer of Record (IOR) themselves. It is no longer feasible to nominate another entity merely in name as the importer.

In instances other than normal import transactions between an overseas seller and a Japanese buyer, where the importer does not have the authority to dispose of the goods after importation (for example, when a foreign corporation does not become the IOR themselves and nominates a forwarder, customs broker, or another third party who is not involved in the transaction to be the nominal IOR), there is a high probability that approval will not be granted as such nominations are not recognized as legitimate importers, necessitating caution.

Notably, foreign corporations that act as importers themselves, through the engagement of ACP, are eligible for Japan Consumption Tax (JCT) benefits. (link: Consumption Tax Treatment and Benefits of Using ACP).

As a dedicated ACP firm, we ensure compliance with the law to facilitate correct import procedures, allowing you to trust us with your importation requirements confidently. We are eager to engage in further discussions with you.

Revisions Effective October 1, 2023:

Definition of the Importer

- Regarding a cargo imported under import transaction, an importer is equivalent to “a person who imports a cargo” defined in Article 6-1 (1), General Notification of the Customs Act. ….. This means, the Consignee, etc., in the case of imports conducted through normal transactions between an overseas seller and a Japanese buyer

- In the cases other than above, an importer is a person who has a right to disposition of the import cargo at the time of import declaration. If there is another person who acts on the purpose of the import*, that person is also included :

In case of a cargo imported:

– under lease contracts, a person who rents and uses the cargo.

– for consignment sales, a person who sells the cargo in the name of himself/herself (consignee) by accepting the commission.

– for processing or repairing, a person who processes or repairs the cargo.

– for disposal, a person who disposes the cargo.

For additional information, please refer to the following resources:

Case Study: Directives to use ACP

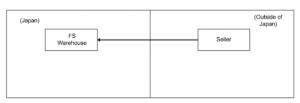

Case 1: Importing Goods Using FS (Fulfillment Services) by Non-resident Sellers

A non-resident seller plans to import goods for sale domestically using FS provided by EC platform operators. At the time of import declaration, there is no sales contract between the seller and the consumer. The seller (non-resident) is the main entity for sales on the EC platform after domestic pickup of the goods. Therefore, the seller, who aims to sell the goods in accordance with the purpose of import, needs to become the import declarant and appoint Attorney for Customs Procedure (ACP) to carry out the import declaration.

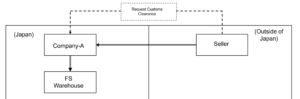

Case 2: Importing Goods Using FS by Non-resident Sellers

A non-resident seller plans to import goods for sale domestically using FS provided by EC platform operators. At the time of import declaration, there is no sales contract between the seller and the consumer. The seller (non-resident) entrusts domestic customs clearance arrangements to Company-A (located in Japan), but the main entity for selling the goods within the domestic market using FS remains the seller (non-resident). It is planned that the seller (non-resident), who intends to sell the goods on the EC platform after domestic pickup, should become the import declarant and appoints Attorney for Customs Procedure (ACP) in accordance with the purpose of import declaration.

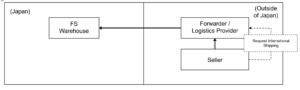

Case 3: Importing Goods Using FS by Non-resident Sellers

A non-resident seller plans to import goods for sale domestically using FS provided by EC platform operators. At the time of import declaration, there is no sales contract between the seller and the consumer. The seller (non-resident) entrusts the transportation of the goods from overseas sellers to Japan to an overseas forwarder, but the main entity for selling the goods within the domestic market using FS remains the seller (non-resident). It is planned that the seller (non-resident), who intends to sell the goods on the EC platform after domestic pickup, becomes the import declarant and appoints Attorney for Customs Procedure (ACP) in accordance with the purpose of import declaration.

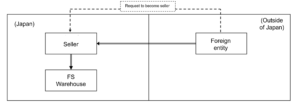

Case 4: Importing Goods for Consignment Sales

Goods (consignment sales goods) intended for domestic sale by an assignee who has received consignment sales from a non-resident consignor are imported. The imported goods are stored in an FS warehouse and sold on the EC platform under the name of the assignee. The assignee is the main entity for selling the goods within the domestic market using FS.

Either of the following options is necessary:

The consignor (non-resident) who has the authority to dispose of the consignment sales goods becomes the import declarant, appoints Attorney for Customs Procedure (ACP), and carries out the import declaration.

The assignee (i.e., the seller on the EC platform) who conducts the act of selling on behalf of themselves as the purpose of import becomes the import declarant and carries out the import declaration.

For more information regarding the revised regulations by the Japan Customs, please refer to the following:

(Link: Revision of Import Declaration Items and Attorney for Customs Procedure (ACP) System) Ministry of Finance, Japan Customs July 2023 With the expansion of cross-border e-commerce, the importation of goods for online shopping has increased, leading to a significant number of cases involving the smuggling of illegal drugs and counterfeit goods that infringe upon intellectual property rights. Particularly concerning are instances of tax evasion, where goods imported through fulfillment services (FS) are declared at unreasonably low prices to evade customs duties.

In light of these circumstances, we have conducted a review of the existing system to ensure the continued facilitation of smooth imports while effectively combating smuggling activities and ensuring proper taxation. Effective from October 1, (2023), there will be an addition to the import declaration items under the Customs Law Enforcement Order, requiring the inclusion of the “address and name of the person intending to import the goods” at the time of import declaration.

Furthermore, there will be additions to the declaration items for Attorney for Customs Procedure (ACP), including information regarding the relationship between the declarant and the Attorney for Customs Procedure (ACP). Additionally, it will be mandatory to submit the contractual documents between the declarant and the ACP. For specific details regarding the revisions to the system, please refer to the following reference materials.

Reference (Japan Customs)

・Leaflet: “Review of Import Declaration Items and ACP system

・Case Study: “Clarification of the Significance of Import Declarants”

・Revision of the ACP Application Form

Our Customers – Japan IOR / Attorney for Customs Procedures (ACP) Service

All our clients have successfully become Japan Importer of Record (IOR) and imported goods into Japan under our guidance.

Logistics Companies with Collaboration Experience

Here is a list of our partner logistics and forwarding companies with whom we have had successful collaborations. Please note that this list is not exhaustive, as we are open to working with any logistics or forwarding companies. As Attorneys for Customs Procedures (ACP), we represent non-resident clients (IOR) and coordinate with these logistics companies, who manage the transportation of goods to and from Japan.

Why choose us?

- Customs and International Trade Professionals – Our CEO, Mr. Sawada, is a Certified Customs Specialist in Japan. With years of experience providing services in the Trade & Customs field, his leadership at KPMG and the establishment of his own company, SK Advisory, ensures our commitment to excellence and high-quality service.

- Full Adherence to Japanese Customs Law – Our top priority is to maintain full compliance with Japanese Customs Law and safely import / export our clients’ goods into / from Japan. We meticulously manage all import compliance aspects, including Japan Importer of Record (IOR) matter, HS code classification and the correct Customs Valuation of goods entering Japan. We support to complete all the necessary shipping documents, such as Invoice, Packing List and BL, on behald of non-resident / foreign Japan IOR.

- Communication in English, Chinese, and Japanese – Our team, with extensive international experience, excels in communication in English, including facilitating English-language meetings, and has earned considerable trust from clients. We also have staff capable of communicating in Chinese, making us equipped to handle Chinese-language support as well. Naturally, as a Japan-based team, we’re totally fluent in Japanese, ensuring seamless communication across these three key languages.

- Reputable and Reliable Partner -The growing demand for our Attorney for Customs Procedures (ACP) services is testament to our quality. We proudly serve clients globally, registering over 50 ACP customers annually. Our consistent track record underscores our reliability and credibility. Our unwavering commitment ensures all our clients successfully acquire Japan IOR status and import goods seamlessly into Japan.

- Handling Regulated Products – Our ACP/IOR partnership system can manage regulated items, including cosmetics, PSE-products, foodstuffs, and tableware.

- Recognized ACP Service Provider on Amazon SPN (Service Provider Network) – We are a certified ACP service provider within Amazon’s Service Provider Network (SPN), listed under the Trade Compliance category. Many international Amazon Sellers have successfully become Japan Importers of Record (IOR) through our ACP services.

Please Be Careful

In cases where foreign corporations (non-residents) without an office in Japan import goods, failure to properly prepare an Importer of Record (IOR) through an Attorney for Customs Procedures (ACP) or similar means can result in goods being held at customs, leading to significant delays and costs. To avoid such risks, please make thorough preparations.

If an ACP is needed, it is crucial to utilize the services of an experienced ACP well-versed in customs-related laws and regulations. The import and export operations of non-residents/foreign corporations using an ACP are treated as unique cases. Many customs brokers are not familiar with these procedures, leading to incidents where goods are detained for extended periods due to unsuccessful explanations to customs. (Customs will not permit the import if the explanations provided by the importer or customs broker are unsatisfactory, resulting in the goods being detained until customs is convinced.)

We highly recommend utilizing our services as professional experts in customs, knowledgeable about customs-related laws and regulations. With a proven track record of resolving numerous issues through direct consultations with customs officers and customs brokers, our clients supported as an ACP now exceed 100 companies. We are committed to delivering industry-leading results with our expertise.

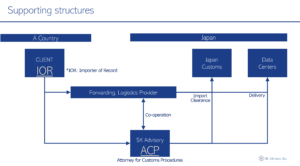

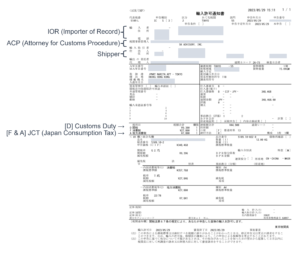

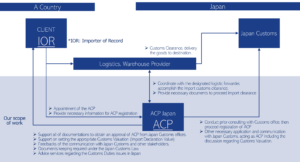

Our ACP Service: The Best Solution for the Japan Importer of Record (IOR) and Exporter of Record (EOR)

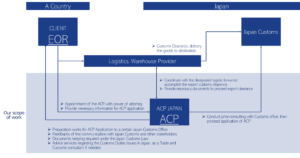

Attorney for Customs Procedures (ACP) is the best solution for addressing the issue of Japan IOR – Importer of Record. Below is an outline of our primary services and a diagram illustrating the operational structure of the ACP service. Upon successful ACP registration, a foreign entity can become the Japan IOR – Importer of Record.

Basic Scope of Services:

- Consultation with the Japan Customs Office for successful ACP registration.

- Liaising with stakeholders, including Logistics Forwarding Companies and the Customs Offices, on behalf of non-resident clients (i.e., non-resident Japan IOR) to ensure the secure importation of goods.

- Assistance in preparing the necessary documentation for import clearance.

- Support of calculation of Customs Value (Customs Valuation Formula), in accordance with appropriate compliance under the Japan Tariff Customs Law.

- Security Export Control (Classification for List Control, Examination for Catch-All Control, Application of the license to Ministry of Economy, Trade and Industry)

- Documents keeping, required under article 95 – Japan Customs Law

- Providing professional trade/customs advice if any issues arise.

**Both import and export activities can benefit from the use of an ACP (Attorney for Customs Procedures). This support is applicable in scenarios where a non-resident acts as the Importer of Record (IOR) for imports and as the Exporter of Record (EOR) for exports.

Three Steps to Initiate Shipments Under the ACP Program: :

- Quotation Review to Contract Conclusion: Upon receiving your contact details, we will promptly provide a quotation for your review.

- Commencing the Registration of ACP (Attorney for Customs Procedure) to Japan Customs: This process is generally completed in about two weeks.

- Initiation of First Shipment, Import/Export

Limitations of Using ACP for Specific Goods by Foreign Japan IOR – Our System Enables Us to Handle Regulated Items

Japanese Certain laws, such as the Pharmaceutical and Medical Products Act, the Electrical Appliance and Material Safety Act (PSE), the Consumer Product Safety Law (PSC), and the Food Sanitation Act, stipulate that importers must be corporations with a registered address in Japan, and thus restrict handling.

However, we have established a partnership system that enables us to arrange the Importer of Record (IOR) and Attorney for Customs Procedures (ACP) for regulated items, including cosmetics, PSE-regulated products, foodstuffs, and tableware.

While many ACP service providers do not handle such regulated items, our ability to handle those regulated items has become a competitive advantage of our company. Please consult with us for handling these regulated items.

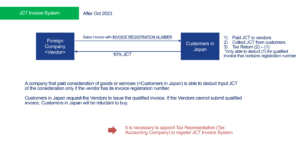

Japan Consumption Tax (JCT) Compliance

Understanding the handling of JCT (such as payment of import JCT, collection of sales JCT from customers, and JCT returns) is crucial to avoid significant cost burdens. This is a vital aspect, so please ensure a thorough understanding to determine the most optimal business model.

Basic Process of JCT Handling

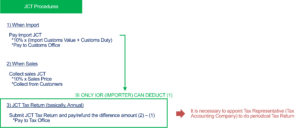

The JCT treatment for foreign corporations without a base in Japan, importing and then selling in Japan, can be broadly outlined in the following three steps:

- At Import: Pay import VAT (10% of the declared value) to customs – Supported by ACP (Attorney for Customs Procedures)

- At Sale: Collect VAT (10% of sales) from customers

- Final Tax Return (usually annually): Deduct the import VAT paid (step 1) from the JCT collected from customers (step 2), and pay or receive the difference to/from the tax office – Supported by a Tax Representative (Certified Tax Accountant)

Note: Using ACP to become the importer (IOR) is essential for JCT deductions and refunds. If another company acts as the IOR, you cannot deduct the input tax (step 1), and must pay the entire VAT collected (step 2) to the national tax authorities, leading to significant costs.

If you are a JCT-exempt business, the process ends at steps 1 and 2. For taxable businesses or invoice-registered businesses, step 3 (Final Tax Return) is obligatory.

In the Final Tax Return (step 3), if the JCT paid (step 1) exceeds the provisional JCT received (step 2), the difference is refunded. Conversely, if the provisional JCT received (step 2) exceeds the JCT paid (step 1), the difference must be paid to the tax office.

Is Being the Importer Important?

It is very important. Without acting as the importer (IOR) through ACP (Attorney for Customs Procedures), you cannot deduct input tax in step 3. You must pay the full amount of JCT collected in step 2 to the tax office, with no possibility of a refund, resulting in substantial costs. Be careful not to let another company act as the importer.

Are we a Tax-Exempt Business?

Tax Payment Obligations of Nonresidents and Foreign Corporations

First, the consumption tax received from customers in Step 2 above should basically be paid to the national tax office. Consumption tax is imposed on transfers, etc. of assets made in Japan. Therefore, even if a nonresident or foreign corporation transfers assets in Japan, it is subject to consumption tax and is obligated to pay the tax.

In some cases, such as exempt businesses, it may not be necessary to pay the tax to the national tax office.

However, the following are examples where one cannot qualify as an exempt business and must file for consumption tax:

<Typical examples of businesses that are not tax-exempt and are required to file a consumption tax return

- Qualified JCT Invoice Issuer

- Businesses with taxable sales exceeding 10 million yen in the base period (roughly speaking, the fiscal year two years prior) for the taxable period

- Businesses with taxable sales exceeding 10 million yen for the specified period (roughly speaking, the first six months of the previous fiscal year, etc.)

- Newly established corporations (including specified newly established corporations) with capital or investments of 10 million yen or more for taxable periods without a base period

- Businesses that have made the election to become a taxable enterprise

※ With the amendments to the Consumption Tax Law in April 2024, regarding point 4, if a foreign corporation has capital or contributions exceeding 10 million yen when they start business operations in Japan (including specifically newly established corporations), regardless of when the corporation was established abroad, they are obliged to pay taxes and declare from the fiscal year they start operations in Japan (applicable for taxable periods starting after October 1, 2024).

Can Tax-Exempt Businesses Receive Refunds?

Yes, it’s possible, but a final tax return (step 3) is necessary. Even if you’re an exempt business, you are still able to opt to submit a “Taxable Business Selection Notification” to the tax office, intentionally becoming a taxable business to file a final tax return and receive a refund for the paid import JCT. This is applicable only if the JCT paid at import (step 1) exceeds the provisional JCT collected (step 2). Note that using an ACP (Attorney for Customs Procedures) to act as the importer is essential for input tax deduction and refunds.

Is It Better to Become a Registered Invoice Issuer?

This depends on individual circumstances, but generally speaking, for B2B where customers are corporations, it’s better to be a Registered Invoice Issuer (as corporations file JCT returns and need qualified invoices for input tax deductions). For B2C where customers are primarily consumers, the necessity is somewhat reduced (as most consumers do not file JCT returns).

Many companies seem to become Registered Invoice Issuer without fully understanding the system. Being a registered business mandates the filing of a final tax return (step 3). Please seek advice from appropriate experts.

Is Support from a Certified Tax Accountant Necessary?

For non-residents conducting tax office procedures (step 3) in Japan, appointing a Tax Representative is required. The ACP handles customs procedures, while the Tax Representative deals with national tax (tax office) matters. Under the Certified Tax Accountant Act, the following tasks are exclusively performed by the Certified Tax Accountants, making their support essential:

- Preparation of tax documents

- Tax representation

- Tax consultation

Our company, in partnership with Certified Tax Accountants skilled in international taxation, will provide support in these areas.

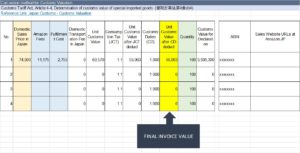

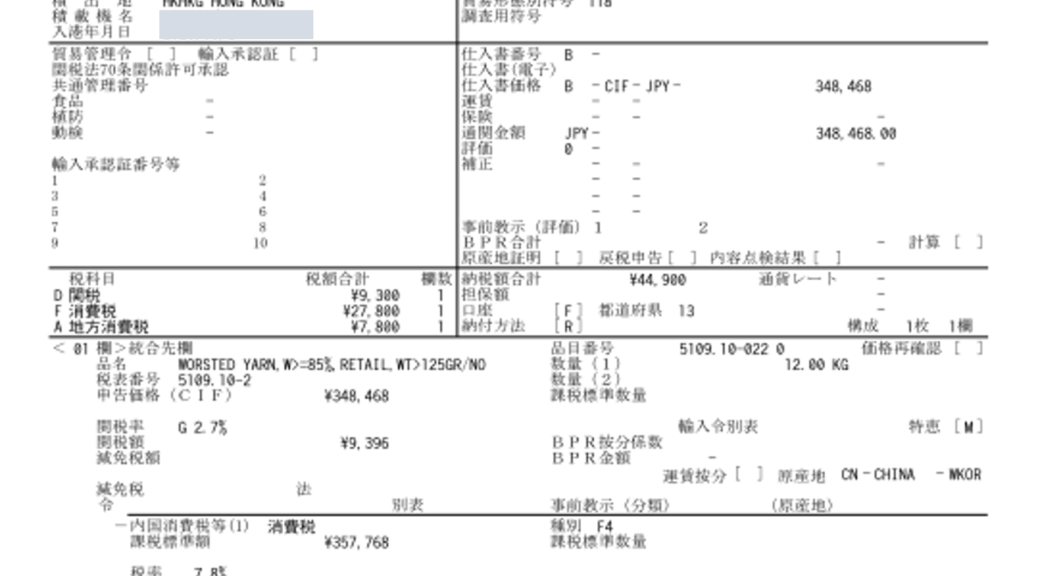

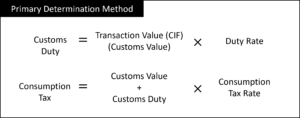

How to determine the Import Declaration Value?

Primary determination method

The process of determining the Import Declaration Value of imported goods is known as “Customs Valuation.” In most cases, when an import is based on an “Import Transaction”※1 between an overseas seller and a buyer in Japan, the primary determination method can be utilized.

※1:An “Import transaction” refers to a transaction where a buyer in Japan engages in a sales transaction with an overseas seller for the purpose of shipping goods to Japan, and the goods subsequently arrive in Japan.

Under the primary determination method, the Customs value of the imported goods is determined as the transaction price paid by the buyer (CIF basis).

Customs Duty is calculated by multiplying the Customs Value (Transaction Value) by the Duty Rate, which varies depending on the HS code of the goods.

Consumption Tax, on the other hand, is calculated by multiplying the Customs Value plus Customs Duty by the Consumption Tax rate (currently 10%).

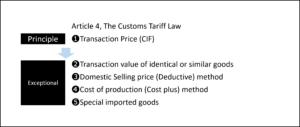

Exceptional determination method (e.g. when to use ACP)

In cases where a non-resident company imports goods into Japan without engaging in a sales transaction, the primary method cannot be utilized. Simply using an Invoice Value is not appropriate.

To calculate the Customs Value in such situations, it is necessary to apply the Exceptional Determination Method.

Within the exceptional determination method, several methods can be considered:

- Transaction Value of Identical or Similar Goods Method: If you have previously imported goods that possess identical or similar conditions to the goods in question, the transaction value of those goods can be used.

- Domestic Selling Price Method (Deductive Method): If you can identify the sales price (can be an estimated sales price), the domestic selling price method can be employed.

- Cost of Production Method (Cost plus Method): If the exporter is a manufacturer and can provide production costs, the production cost method may be applicable.

If none of the above methods are suitable, “Other methods” are utilized as a flexible determination method, taking into account the calculation methods mentioned earlier.

In the practical scene, most of the cases we use this “Other methods” which is a determination method in a flexible way through considering the previously mentioned calculation methods.

Avoiding Customs Valuation Problems

In recent times, there have been numerous instances of trouble arising from incorrect Customs Value settings.

In the worst-case scenario, goods may fail to clear customs, resulting in significant detention fees and eventual return shipment.

At ACP Japan, we specialize in establishing appropriate Customs Values. We can assist in conducting consultations with Japan Customs on behalf of our clients, effectively avoiding any potential issues down the line.

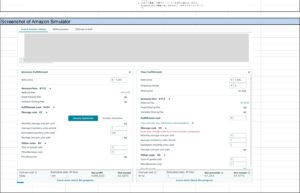

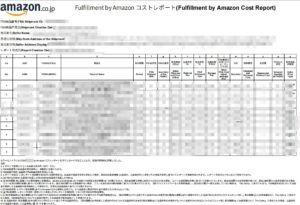

For Amazon’s FBA business, there is a recommended calculation formula for the declaration value. If you would like to learn more about it, please don’t hesitate to contact us!

FAQ for ACP (Attorney for Customs Procedures)

What is the role of ACP (ACP Japan)?

- Representation: ACP (ACP Japan) represents the foreign importer and liaises with Japan Customs and the Forwarding Company/Customs Broker.

- Documentation and Compliance: ACP assists in preparing essential import documents (e.g., Invoices) in compliance with Japan Customs Law and formally requests the Customs Broker to proceed with customs clearance.

- Expert Consultation and Troubleshooting: We are a team of legal experts in Customs Laws, providing direct consultations with Japan Customs to ensure compliance and address issues, including troubleshooting unique challenges in non-resident imports.

How long time does it require to get ACP’s registration?

It will take approximately 2 weeks until getting an approval from Japan Customs Office.

The breakdown of the task is as follows.

- Prepare the necessary documentation between us

- Start pre-consultation with Japan Customs Office and proceed initial review

- Submit paper-based set of application documents to Japan Customs Office for final review

What kind of documents to be necessary for ACP application?

Not limited, but for instance – Power of Attorney, Company Registry, The calculation method of Customs Valuation, Catalog of the import goods, business/logistic flow

ACP can handle all kinds of goods?

Whereas many ACP service providers do not handle regulated items, our company’s competitive advantage stems from our ability to manage such products. We can support regulated items, including cosmetics, PSE-regulated products, foodstuffs, and tableware.

Which regions in Japan are we covering?

Any region in Japan, we can handle.

What is difference between ACP and IOR?

ACP is not the Importer. ACP enables non-resident entities to become IOR (Importer of Record).

Contact us

—–

[Our Service]

Our ACP Service for Importer of Record (IOR)

Our ACP Service for Exporter of Record (EOR)

[Knowledge Pages]

What is ACP? – Attorney for Customs Procedures

Steps of using ACP, how foreign entity can import into Japan by ACP

What is IOR? – Importer of Record

Amazon won’t become an IOR

Customs Valuation System in Japan

Customs Valuation When You Import By ACP

Consumption Tax in Japan

IOR and ACP

IOR Service

Limitation on Handling by ACP in Japan – Our System Enables Us to Handle Regulated Items

ACP’s Qualification

ACP’s registration

[Recent Updates]

Urgent Compliance Alert for E-Commerce Sellers: Avoid Penalties with Japan’s New Import Regulations – Act Now!

October 2023: Introduction of Two New Systems in Japan – (1) Switching from IOR Provider to ACP & (2) QIS: Japan Consumption Tax’s Qualified Invoice System

ACP Japan Became Amazon’s SPN Provider as Qualified ACP Service Provider

Taxes on Imports: Customs Duty and Japan Consumption Tax (JCT)

Import Permit Document and Alert on IOR Service

New Japan Qualified Invoice System and import JCT (Japan Consumption Tax)

Guidance by Amazon

According to the seller central website in Amazon, there is guidance by Amazon that a non-resident entity needs to appoint an ACP or IOR. You may check on this link:

Non-resident requirements

A Fulfillment by Amazon (FBA) seller who lives outside of Japan (non-residents) and would like to import goods into an Amazon Japan fulfillment center for storage and order fulfillment must first designate an Import of Record (IOR) and /or Attorney for Customs Procedure (ACP). This must be accomplished in advance of any importations. In general, any person who is a resident of Japan can be appointed as an IOR and/or ACP. Neither Amazon nor any of its entities in Japan may act as the IOR/ACP on the customs declaration, only the FBA seller or their designated IOR/ACP.

Amazon, Seller Central, Japan Tax and Regulatory Considerations

Also, you can check the document developed by Amazon “Understand ACP and IOR guidance”.

Understand ACP and IOR

If you do not have a Japanese entity to act as the importer of record, it is mandatory that you appoint an Attorney for Customs Procedure (ACP). Overseas Sellers, as non-resident importers, can generally rely on a program called ACP to help bring their inventory into Japan. An ACP is a resident Japanese entity who registers with Japan Customs as your agent to help with entries and communications. Please note ACP does not fully take over the whole responsibility of an importer. You must ensure that your goods comply with the local laws and regulations as a part of your responsibility.

Amazon, Understand ACP and IOR guidance

Recently, Amazon issued another guidance regarding the Understanding of Attorney for Customs Procedures (ACP) in accordance with the new Japan Customs Regulations that have been effective since October 2023.

Understand ACP/CPA

To import your FBA shipment, you may need an ACP (Attorney for Customs Procedures, also called Customs Procedure Agent or CPA; hereinafter ‘CPA’) to support the customs clearance

procedures for your goods. The following materials on the Japan Customs website explains in what situations you need a CPA.

https://www.customs.go.jp/shiryo/jirei.pdf

If you are required to use a CPA, Overseas FBA sellers will be filing import declarations under the seller’s name while using a CPA to help bring their inventory into Japan. A CPA is a resident Japanese entity who registers with Japan Customs as your agent to help with customs declarations and communications. Please note CPA does not fully take over the whole

responsibility of an importer. You must ensure that your goods comply with the local laws and regulations as a part of your responsibility.

Please note that the customs territory of Japan is divided into regional areas that do not share information regarding CPA registration. This means you can only rely on your CPA in the region(s) where the application is received. You have to appoint a CPA in each region if necessary. Once you find out the destination Fulfillment Centre (FC) for your goods, please ensure that your CPA is registered in all required regions. For details, you should consult with the relevant customs office.

Are certain product categories limited to Japanese-resident as Importer instead of an ACP/CPA?

There are certain products that are subject to notification, certification, or registration requirements that must be met by a resident Japanese entity who is also responsible for ensuring

the imported goods comply with local laws and regulations. Because these requirements can only be met by a Japanese entity, a non-resident IOR cannot meet them. You are responsible for determining whether or not your goods require a notification, certification, or registration. Japan Customs website has provided an outline of relevant laws and ordinances as a guide but you should also consult with your customs broker or legal advisor. Additionally, all imported products must meet Japanese regulations and product labeling obligations.

For more information, please refer to the Japan Customs’ website: http://www.customs.go.jp/

For more information on the 2023 Japan Customs Act Amendment, please refer to the Japan

Customs’ website:

[JP] https://www.customs.go.jp/shiryo/leaflet_jimukanrinin.pdf

[EN] https://www.customs.go.jp/shiryo/leaflet_jimukanrinin_e.pdf

[CN] https://www.customs.go.jp/shiryo/leaflet_jimukanrinin_cn.pdf

[KR] https://www.customs.go.jp/shiryo/leaflet_jimukanrinin_kr.pdf