Customs Valuation: Determining the Import Declaration Value

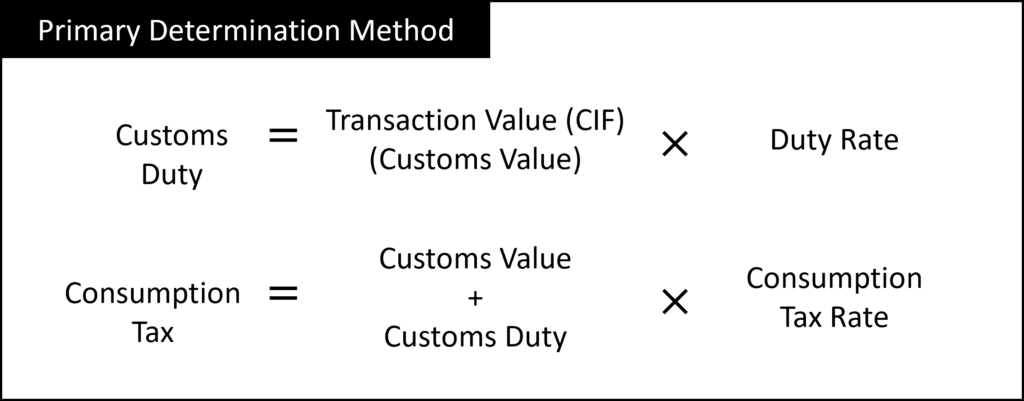

Primary Determination Method

The process of determining the Import Declaration Value of imported goods is known as “Customs Valuation.” In most cases, when an import is based on an “Import Transaction”※1 between an overseas seller and a buyer in Japan, the primary determination method can be utilized.

※1:An “Import transaction” refers to a transaction where a buyer in Japan engages in a sales transaction with an overseas seller for the purpose of shipping goods to Japan, and the goods subsequently arrive in Japan.

Under the primary determination method, the Customs value of the imported goods is determined as the transaction price paid by the buyer (CIF basis).

Customs Duty is often calculated by multiplying the Customs Value (Transaction Value) by the Duty Rate, which varies depending on the HS code of the goods.

Consumption Tax, on the other hand, is calculated by multiplying the Customs Value plus Customs Duty by the Consumption Tax rate (currently 10%).

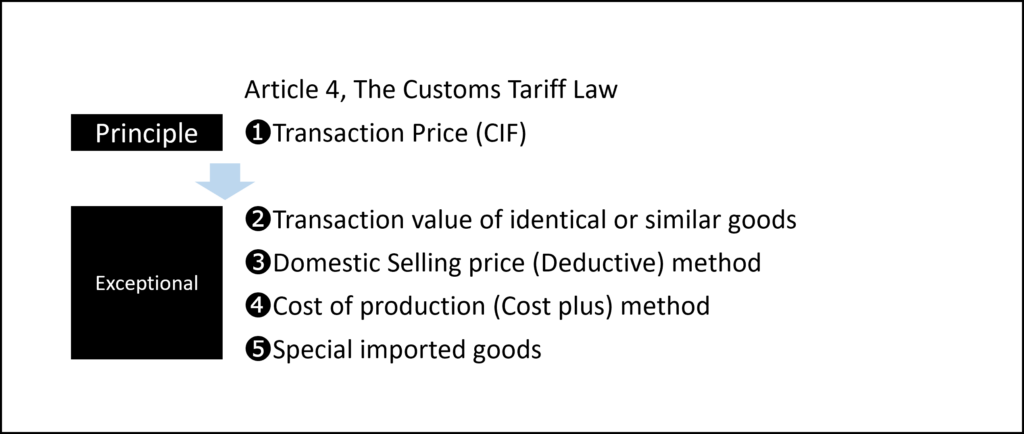

Exceptional Determination Method (e.g. when ACP is required)

In cases where a non-resident company imports goods into Japan without engaging in a sales transaction, the primary method cannot be utilized. Simply using an Invoice Value is not appropriate.

To calculate the Customs Value in such situations, it is necessary to apply the Exceptional Determination Method.

Within the exceptional determination method, several methods can be considered:

- Transaction Value of Identical or Similar Goods Method: If you have previously imported goods that possess identical or similar conditions to the goods in question, the transaction value of those goods can be used.

- Domestic Selling Price Method (Deductive Method): If you can identify the sales price (can be an estimated sales price), the domestic selling price method can be employed.

- Cost of Production Method (Cost plus Method): If the exporter is a manufacturer and can provide production costs, the production cost method may be applicable.

If none of the above methods are suitable, “Other methods” are utilized as a flexible determination method, taking into account the calculation methods mentioned earlier.

In practice, in most cases, we use this “Other Methods” approach, which allows the customs value to be determined flexibly by considering the previously mentioned calculation methods.

Avoiding Customs Valuation Problems

In recent times, there have been numerous instances of trouble arising from incorrect Customs Value settings.

In the worst-case scenario, goods may fail to clear customs, resulting in significant detention fees and eventual return shipment.

At ACP Japan, we specialize in establishing appropriate Customs Values. We can assist in conducting consultations with Japan Customs on behalf of our clients, effectively avoiding any potential issues down the line.

For Amazon’s FBA business, there is a recommended calculation formula for the declaration value. If you would like to learn more about it, please don’t hesitate to contact us!

Customs Value Affects Import Taxes

The customs value directly impacts the amount of import taxes. That said, Japan’s low tariff rates mean that valuation primarily affects the Japan Consumption Tax (JCT) rather than customs duties. As noted, if you are properly registered as the Importer of Record (IOR) and have appointed a JCT Tax Representative, the JCT is recoverable and not a cost to your business. Therefore, there is generally no need to be overly concerned about the declared value.

Import Taxes: Customs Duties and JCT

There are two main types of import taxes in Japan:

▶ Customs Duty:

Tariff rates vary depending on the HS code; however, most industrial products are either duty-free or subject to low rates in Japan. You can check tariff rates at Japan Customs Website: JP Tariff Rates

▶ Japan Consumption Tax (JCT):

JCT is set at a fixed rate of 10%. JCT is calculated as 10% of the total import declaration value plus customs duty. For more detailed information about JCT, please visit our webpage: Consumption Tax

Tax Filing and Payment to the Tax Office

After importing goods, you are allowed to collect 10% Japan Consumption Tax (JCT) from customers upon domestic sales. If you are a JCT-exempt entity, no further action is required.

If you are a JCT-taxable entity, you must file a JCT tax return with the local tax office and pay the collected sales JCT. During this process, you may deduct or claim a refund of the JCT paid at the time of import.

Only the Importer of Record Can Claim Input Tax Credit

The right to claim an input tax credit for import JCT belongs exclusively to the Importer of Record (IOR). This is why appointing an Attorney for Customs Procedures (ACP) is critical. If the foreign company does not act as the importer—such as when a third party is listed as the IOR—the company may lose the right to reclaim the import JCT, resulting in a significant financial loss.

Compliance with the Japanese Invoice System

Since October 2023, Japan has implemented a new JCT Invoice System, similar to the European VAT compliance framework. Foreign sellers must consider whether to register as a Qualified Invoice Issuer, particularly when selling to JCT-registered buyers in Japan. If a foreign seller is not registered as a Qualified Invoice Issuer, the buyer may be unable to fully claim input JCT through their JCT tax return.

To maintain good business relationships, it is often advisable to register proactively. However, once registered as a Qualified Invoice Issuer, you can no longer be treated as a tax-exempt entity and must begin filing and paying JCT accordingly.

Necessary to Appoint a Tax Representative

To complete this process—registration and JCT filing—a Tax Representative (usually a certified Japanese tax accountant) must be appointed separately from the ACP.

We work closely with trusted tax professionals to provide comprehensive, one-stop support for both ACP and JCT Tax Representative services.

Why choose us?

We specialize in navigating complex issues at the intersection of customs procedures and taxation—an area where our ability to offer practical, comprehensive support from both perspectives sets us apart. Understanding the close relationship between customs duties and national taxes (especially, Japan Consumption Tax – JCT), and addressing both in an integrated manner, is crucial in the context of international trade.

- Customs and International Trade Professionals – Led by our CEO, Mr. Sawada—Certified Customs Specialist and former KPMG professional—ACP Japan provides expert-level support in Customs and international trade. Mr. Sawada also serves as an external expert for the World Bank’s B-READY project in the field of customs and international trade.

- Full Compliance with Japanese Customs Law – We ensure full adherence to Japanese Customs Law, including Importer of Record (IOR) structure, HS code classification, and customs valuation. We assist in preparing all essential shipping documents for non-resident entities.

- One-Stop ACP and JCT Tax Representative Service – We offer a fully integrated service for both ACP and JCT Tax Representative needs. Our expertise enables efficient deduction or refund of import JCT through accurate JCT tax filings.

- Multilingual Communication – Our team communicates fluently in English, Japanese, and Chinese, offering smooth coordination with global clients and authorities in Japan.

- Support for Regulated Products – Our ACP/IOR partnership system can manage regulated items, including cosmetics, PSE-products, foodstuffs, and tableware.

- Trusted by Global Clients – Serving around 100 ACP clients annually, including many Amazon sellers, we’re a certified provider on Amazon SPN (Service Provider Network) under Trade Compliance.

Track Record – Attorney for Customs Procedures (ACP) Services

We have supported import and export operations in Japan for over 200 clients across more than 40 countries.

Examples of International Logistics Partners We Have Worked With

We have a proven track record of working with a wide range of logistics providers. As the Attorney for Customs Procedures (ACP), we handle customs-related responsibilities while logistics companies manage transportation and warehousing operations.

- American Overseas Transport (AOT)

- Apex International

- Brink’s

- CEVA Logistics

- Coshipper

- Crane Worldwide Logistics

- DB Schenker

- DGX (Dependable Global Express)

- DHL Express

- DHL Global Forwarding

- Dimerco

- DSV Air & Sea

- Expeditors

- FedEx Express

- FERCAM

- GOTO KAISOTEN Ltd.

- Harumigumi

- Herport

- ICL Logistics

- JAS Forwarding

- Kintetsu Express

- Kokusai Express

- Kuehne + Nagel

- Mitsubishi Logistics

- MOL Logistics

- Nankai Express

- Nippon Express

- OIA Global

- PGS

- Rhenus Group

- Röhlig

- Sankyu

- Sanyo Logistics

- Scan Global Logistics

- Seino Schenker

- SEKO Logistics

- Shibusawa Logistics Corporation

- Shin-Ei gumi

- Shiproad

- Sumitomo Warehouse

- UPS

- UPS Supply Chain Solutions

- Yamato Transport

…and many other logistics providers in Japan and around the world.

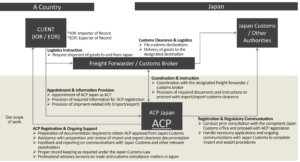

Our ACP Service : The Best Solution for the Japan Importer of Record (IOR) and Exporter of Record (EOR)

ACP is an effective solution for addressing Importer of Record (IOR) and Exporter of Record (EOR) requirements in Japan. Through our ACP service, non-resident entities located outside Japan are able to import and export goods as Non-Resident IOR and EOR.

Below is an overview of our basic scope of work, together with a diagram illustrating the operational structure of the ACP service. Once ACP registration is completed, the non-resident entity can act as the Importer of Record (IOR) and Exporter of Record (EOR) in Japan.

Scope of Work – How We Can Assist

- Consultation with Japan Customs to support successful ACP registration.

- Liaison with relevant stakeholders, including freight forwarders and Japan Customs, to ensure the smooth and compliant import and export of goods.

- Assistance in preparing and reviewing import and export clearance documentation.

- Support in the calculation of customs value, in accordance with the Japan Customs Tariff Act.

- Assistance with advance rulings on HS classification, customs valuation, and rules of origin.

- Import compliance support for regulated products, including Domestic Administrator (sometimes referred to as “Domestic Representative”) Services under the Product Safety Acts (PSE/PSC) and food-related products regulated under the Food Sanitation Act.

- Support for security export control, including list-based classification, catch-all control assessment, and assistance with export license applications to the Ministry of Economy, Trade and Industry (METI).

- Record-keeping support in accordance with Article 95 of the Japan Customs Law.

- Provision of professional trade and customs advisory services to address and resolve issues that may arise during import or export operations.

**Both import and export activities can benefit from the use of an ACP (Attorney for Customs Procedures). This support is applicable in scenarios where a non-resident acts as the Importer of Record (IOR) for imports and as the Exporter of Record (EOR) for exports.

Three Steps to Initiate Shipments Under the ACP Program:

-

Quotation Review to Contract Conclusion: Upon receiving your contact details, we will promptly provide a quotation for your review.

-

Commencing the Registration of ACP (Attorney for Customs Procedure) to Japan Customs: This process is generally completed in about two weeks.

-

Initiation of First Shipment, Import/Export

FAQ for ACP (Attorney for Customs Procedures)

What is the role of ACP (ACP Japan)?

- Representation: ACP (ACP Japan) represents the foreign importer and liaises with Japan Customs and the Forwarding Company/Customs Broker.

- Documentation and Compliance: ACP assists in preparing essential import documents (e.g., Invoices) in compliance with Japan Customs Law and formally requests the Customs Broker to proceed with customs clearance.

- Expert Consultation and Troubleshooting: We are a team of legal experts in Customs Laws, providing direct consultations with Japan Customs to ensure compliance and address issues, including troubleshooting unique challenges in non-resident imports.

How long does it take to complete ACP registration?

It will take approximately 2 weeks until receiving approval from Japan Customs. The breakdown of the task is as follows.

- Prepare the necessary documentation in coordination between the client and ACP Japan

- Start pre-consultation with Japan Customs and proceed with the initial review

- Submit a paper-based set of application documents to Japan Customs for final review

What documents are required for ACP application?

For example, but not limited to: a Power of Attorney, company registry documents, the calculation method for customs valuation, product catalogs for the imported goods, and the business/logistics flow.

ACP can handle all kinds of goods?

While many ACP service providers do not handle the regulated items, our ability to handle those regulated items has become a competitive advantage of our company. We can support the items including cosmetics, PSE-regulated products, foodstuffs, and tableware.

Which regions in Japan are we covering?

We can handle shipments to any region in Japan.

What is the difference between ACP and IOR?

ACP is not the Importer. ACP enables non-resident entities to become IOR (Importer of Record).

References

Japan Customs – Customs Valuation System in Japan

Amazon, in seller central website, released the guideline of Customs Valuation.

- Main Trade Procedures and Customs Valuation (English)

- Main Trade Procedures and Customs Valuation (Chinese)

- Main Trade Procedures and Customs Valuation (Japanese)